[ad_1]

We Are

The Global X Alternative Income ETF (NASDAQ:ALTY) looks alright. The dividend record could be a little better, but it is high in yield and gives a lot of fair exposures. Financial preferred shares aren’t bad at all for a sustainable yield. Otherwise, major exposures include REITs. The emerging market bond instruments are less interesting for us, since there’ll be duration risk there, but it comes across as a very safe source of yield.

ALTY Breakdown

60% of the allocation is split evenly between 3 other Global X ETFs:

The first 20% is in a Global X US Preferred ETF (PFFD). This ETF holds substantially financial sector preferred shares. Financials are appropriate for the current market, even banks that have long had to grow their exposure to fee-based income to survive the low-rate environment. The spread between lending rates and savings rates are rising right now, which helps with duration gaps that would otherwise be unfavourable in a rate-hike environment. Savings rates are staying at rock-bottom levels, maybe because people don’t really use their deposit accounts for savings anymore, and have had all their investment money in stock accounts. Preferred shares give you seniority over equity in the capital structure, which reduces risk in theoretical liquidation. Also their value is somewhat driven by fundamentals when there is distress over the preferred dividend, which becomes a company liability when it’s not paid. If fundamentals improve premiums to the discount rate aren’t as present and value can rise. Generally however, there isn’t much capital gains potential. This means that the income from preferred shares are bond-like, and there is duration risk, but it tends to be not as bad for preferred shares.

The other major exposure is in a Global X SuperDividend REIT ETF (SRET). We’ve actually covered SRET separately and we like it. There are plenty of highly resilient specialty exposures within to the sorts of economic declines we expect with this recession. Moreover, REITs as an asset class outperform in uncertain markets, and also when markets inflect into a bull market trend. It’s a great exposure to sit on for the yield as well.

Finally, a lot of exposure comes from an ETF of emerging market bonds. In many instances, they are issued from countries like Brazil that are benefiting in the current commodity environment and are not so affected by pressures from a deteriorating FX. Nonetheless, any bond exposure is going to have duration risks, and rate hikes continue.

Conclusions

The yield exposures look good, albeit with some duration risk on the preferreds and the bonds. Improving fundamentals benefits the preferred exposures for financial firms. The yield from those should be pretty constant. Indeed, the PFFD has very stable distributions. But they won’t grow, because that’s not how preferred dividends work. There is duration risk with the EM bonds, but yield is yield, and it’s not the whole portfolio. Finally, REITs are very solid exposures and have rate increases built into leases to grow distributions.

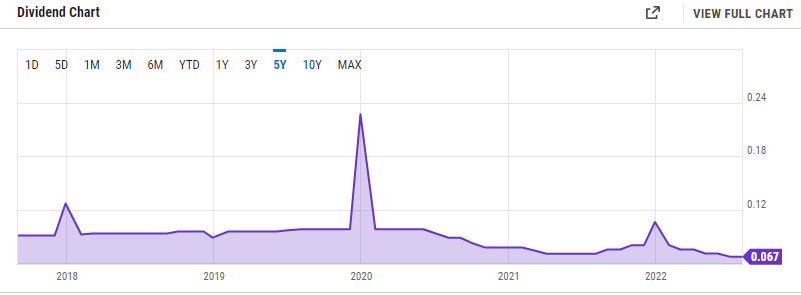

We like ALTY from a fundamental point of view, but the distributions could be more consistent. It’s gone into a bit of a decline over the last 3-4 years.

Dividend (ycharts)

Nonetheless, the yield is solid at 8.2%. We think it’s covered directionally by the exposures. If you want you might consider it.

While we don’t often do macroeconomic opinions, we do occasionally on our marketplace service here on Seeking Alpha, The Value Lab. We focus on long-only value ideas, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, us at the Value Lab might be of inspiration. Give our no-strings-attached free trial a try to see if it’s for you.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.